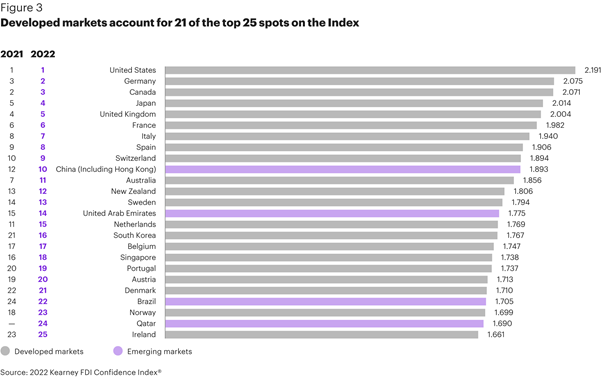

1. Canada third most attractive global destination for FDI according to new survey

Foreign Direct Investment Confidence Index (FDICI) from Kearney’s Global Business Policy Council a new index has named Canada third top foreign direct investment location with only Germany and the US placing higher. The index measures 25 markets and benchmarks markets most likely to attract investment over the next three years. The survey of business professionals showed increasing confidence regarding global economic recovery despite the 35% drop in global FDI in 2020 due to the pandemic.

With the global FDI recovery figure now up 77% on that 2020 figure, it is little wonder optimism is up on 2021. 76% of business leaders surveyed said they would increase FDI over the next three years including 50% in America who cited FDI becoming even more important in the near future. Those results were taken before the war in Ukraine broke out which had a slight dampening on sentiment.

Europe gained top position regionally with 14 economies representing 25% on the list with the United Kingdom fourth after Japan got third spot. Read the full report here.

2. Ireland to commence R&D Tax Breaks Consultation

With the global minimum tax looming Ireland is seeking public comments on an R&D scheme which provides tax relief on intellectual property developed in Ireland. The global minimum tax arrangement was originally proposed in 2021 by the OECD however at this current moment is blocked by Poland (see next article). Ireland’s initiative gives back 25% of what companies spend on R&D in Ireland. This is a very popular scheme with 1,600 companies eligible and claiming in 2019 costing 626 million euros.

Corporate tax in the UK remains uncertain with the Chancellor increasing corporate tax for the first time since 1974 in 2021 from 19% to 25% but with a generous capital allowance scheme which allows companies to claim 130% of plant and machinery – great for the construction industry!

The consultation ends on 30 May.

Trade Horizons

Trade Horizons is an award-winning market entry company, assisting ambitious companies to identify, develop and grow sustainable revenues in new geographic markets. We offer support to clients in international strategy development for their global business growth, and throughout the key phases of market entry execution – Preparation, Launch and Growth. Click here to find out more.

3. Yellen confident U.S. Congress will pass minimum global corporate tax

More on the global minimum corporate tax: US seems on board with Treasury Secretary Janet Yellen confident the deal would be approved but they have struggled to get it through Congress so far. The global minimum corporate tax was first proposed by the OECD and so far, 140 countries have committed to sign up to it (except Poland, see below). Designed to stop large corporates dodging and undercutting on tax with global tax avoidance, base erosion and profit shifting (BEPS), the new deal aims to ‘level the playing field’ providing a low tax threshold for everyone.

Currently two of the three ‘large corporates’ this deal is aimed at being Google, Amazon and Facebook, are headquartered in Ireland. Ireland, Hungary and Estonia were holding out in the previous round of negotiations, but these countries have now all signed. The deal will end Ireland’s 18 year history of the low corporate tax rate of 12.5% which attracted companies such as Google and Facebook to headquarter there. Currently all 38 OECD member countries have agreed with Kenya, Nigeria, Pakistan and Sri Lanka not joining.

The new deal ‘does not eliminate’ tax competition but sets the low bar at 15% on large companies with revenues of more than 750 million euros. There is apparently an extra US$150 billion that the OECD will collect for governments globally. Nigeria and Kenya have declined to join stating the deal disproportionately favours large economies leaving small countries without claim. The reforms were agreed at the G7 summit in London in June with implementation due in 2023. With still a lot of uncertainty surrounding the deal, successful implementation remains to be seen.

3. Poland blocks minimum corporate tax global deal

Poland has blocked the EU’s move to sign up to minimum global corporate tax rate of 15% citing that the deal is not a legally binding solution to assure that countries enter the deal at once. The deal requires unanimous agreement from countries and nations. The EU allowed some nations to commit to implement part of the deal at different times (Pillar I and Pillar II) but Poland said this would enable an unequal playing field, against which Poland is currently contesting. Poland says the two pillars must be implemented at the same time despite some countries not being ‘ready’ meaning probably implementation of the whole deal will be pushed back. The 2023 timeline is seen as highly ambitious given that the US has struggled to only just push it through congress.

Sweden, Estonia and Malta were holding out but have agreed the latest deal.